Super Micro Computer (NASDAQ:SMCI) is a global Information Technology firm headquartered in San Jose, California, United States. In this thesis, I will be covering the groundbreaking Universal Graphics Processing Unit (GPU) systems designed by SMCI, which could be a game-changer for the firm. I will also be analyzing stellar Q3 2022 results by the firm and a strong outlook for the future. I believe SMCI is one of the best stocks in the hardware technology and storage space, both in terms of valuation and significant future growth prospects. I assign a buy rating for SMCI after deeply analyzing its technological innovations as well as impressive quarterly results with a strong future outlook.

About SMCI

SMCI is an IT company specializing in Artificial Intelligence (AI), Cloud Servers, IoT and 5G Telco infrastructure. The company also develops high-volume motherboard and chassis products. The company is transforming itself into a Total IT service provider, providing all the IT solutions at one stop with complete integration through its Universal GPU system. SMCI has a global presence in terms of production as well as sales. The company has 40% of its sales outside the United States, with most of its exports to the European region and China. SMCI has three main production facilities, one each in the United States, Taiwan and the Netherlands. Most of its production is carried out at the San Jose, California, production plant. As the company deals in the large category of hardware and software products, it has several competitors across segments; most notable among them are Dell (DELL), Cisco (CSCO), Foxconn and Quanta Computer. SMCI focuses mainly on Innovation, and hence it is investing heavily in Research and Development to adapt to future technologies in AI and the 5G space. They derive their competitive edge from emerging technologies first in the market.

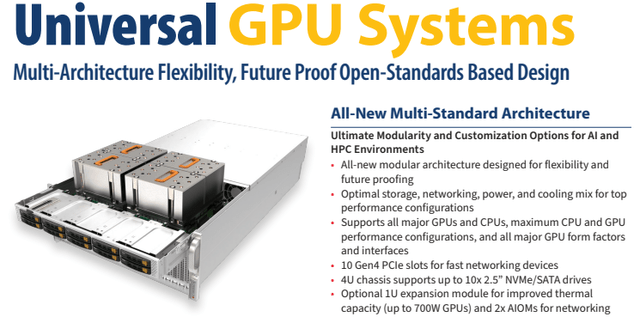

Universal GPU Systems

Investor Relation

SMCI’s Universal GPU system is a pioneering technology which is considered to be one of the most advanced and dynamic GPU server platform in the industry. This platform is designed to manage heavy and deep AI learning and HPC workload. With the increasing use of AI in many sectors, this GPU server platform by SMCI is expected to create a big market for the firm in the near future. One of the most important features of this system is that it is future-proof, meaning it is built to accommodate and support technologies which are expected to come in future. Universal GPU Platform is universal because it is built to work with different GPUs by being standard in design to accommodate various elements. For example, this system supports GPU interconnection between NVIDIA’s (NVDA) NVLink and AMD’s (AMD) Infinity Fabric that facilitates hyper-speed inter GPU communication, reducing bottlenecks caused by traditional GPU interlinks. This is one of a kind product, which as per my analysis, will take up the majority of the revenue share of SMCI by FY24. I believe this is the result of high investment in R&D by SMCI, which the company still continues, which is helping them have the edge over its competitors in terms of technological advancement.

Financials

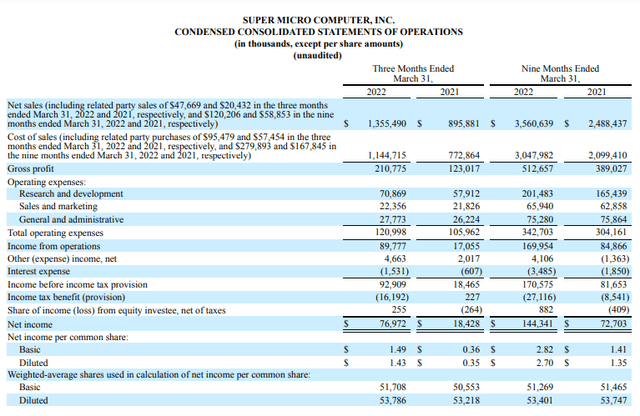

Recently, Super Micro Computer has reported strong Q3 FY22 results. The company has reported net sales of $1.36 billion, which is 52% YoY growth compared to $896 million of Q3 FY21. On a sequential basis, net sales have grown 16.2% QoQ compared to $1.17 billion in the same year’s second quarter. The gross margins have expanded by 1.8% compared to the last year’s period. The company has surprised the market with outstanding net income growth of 327% YoY. Net income and diluted EPS of the current quarter are $77 million and $1.43 per share, respectively, compared to $18 million and $0.50 per share of the previous year’s second quarter. The reported CFO of the third quarter is $228 million, while the capital expenditure is $11 million. The strong result of the company is a reflection of the efficient operational leverage and product optimization.

This is Supermicro’s fourth consecutive quarter of revenues exceeding a billion dollars and with a trailing four-quarter revenue run rate of $4.6 billion, it gives me strong confidence that we are well ahead of our long-term targets. Our robust growth and EPS progress demonstrate the efficiency of our global operational leverage, and our customers recognizing the value of our rack-scale Total IT Solutions in key market segments across AI, enterprise, cloud, edge/telco and others. Along with our product optimization, time to market advantage, and green computing cost-savings presented by our Total IT Solutions, our growth momentum should continue to fuel our emergence as the leading company in the industry in the coming quarters and years ahead.

SEC: 10Q SMCI

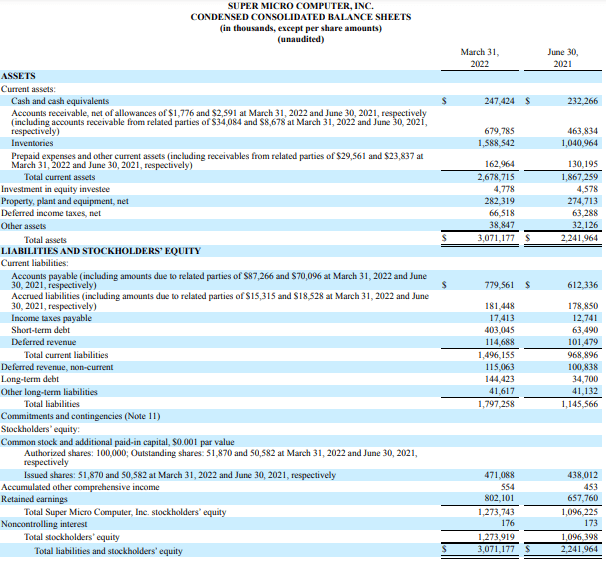

This was all about the income statement. Now let’s discuss the balance sheet. The company has ended Q3 2022 with $247 million in cash and cash equivalents and $547 million in bank debt. In the last year, the inventory of the company has shown a growth of 45%. The rising inventory levels are a sign of the increasing demand of the company.

SEC: 10Q SMCI

After the consecutive strong results, I am estimating a strong coming quarter for the company, and even the management is very optimistic about the fourth quarter. That’s why the company has raised its previous guidance. The company is estimating net sales to be in the range of $1.4 billion to $1.48 billion. The GAAP diluted EPS is estimated to be in the range of $1.45 to $1.64. For the FY 2022, the company has raised its net sales outlook from $4.2 billion -$4.6 billion to $4.96 billion-$5.04 billion, and diluted EPS is estimated to be in the range $4.16 to $4.35. I believe these strong estimates are enough to justify my thesis. I also think the company will exceed these estimates in the current quarter result as generally March ending quarter is considered a weak one and still the company has reported a strong result.

Potential Risk Factors

Impact of Geopolitical Tension: The company deals with many international clients, almost all the big clients of the company are international. Suppose any SMCI client’s country starts a trade war or puts any sanction on imports from the United States. In that case, the company can lose a significant client as most of its revenue stream is dependent on a limited number of international clients. That’s why I believe the company is exposed to geopolitical tensions such as trade wars, tariffs and sanctions in our geographic markets.

Availability of the Key Components: Due to the Covid-19 pandemic, the supply chain of the company and the suppliers has been already disrupted. As we know, the company’s business is dependent on the availability of critical components such as semiconductors, memory, storage solutions, and other materials because the cost of these products fluctuates according to the supply of the parts, which can affect the margins of the company. Currently, the prices of hardware are rising because of the scarcity of the products in the market, which can be risky for the company if it fails to fulfil the client’s orders as per requirement.

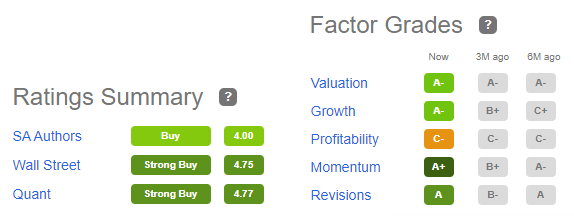

Quant Ratings

Seeking Alpha

The quant ratings of seeking alpha suggests a strong buy for this stock, which clearly indicates that the company is trading in a growing space. According to factor grades, the valuation has the grade of A- which reflects the cheap valuation and momentum has a grade of A+.

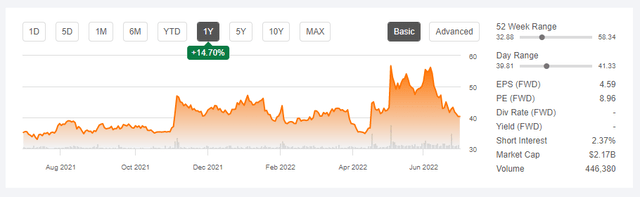

Seeking Alpha

Currently, the company is trading near its 52-low (20% up from 52-low), and I believe with cheap valuation and strong upside momentum in stock price, $40.35 is an optimum entry point for the investors.

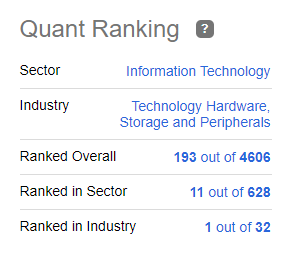

Seeking Alpha

The company is ranked 1st out of 32 companies in the industry. All these factors support and validate my investment thesis.

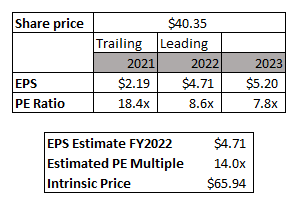

Valuation

PE Model by Author

Currently, the company is trading at $40.35 with a market cap of $2.09 billion and a leading PE multiple of 8.57x. I believe that for a growth company, it is currently trading at a cheap multiple and will trade at a high P/E multiple in coming quarters. SMCI is trading at a cheaper P/E valuation of 11.8x than its main competitors, such as Globant (GLOB) trading at a P/E multiple of 66.56x, Cisco at 14.61x and Foxconn at 15.33x. I believe with the conservative outlook, the EPS of 2022 will be $4.71, and P/E multiple will be 14x, which suggests that the stock’s target price is $65.9, which is a 63.4% upside from the current market price.

Conclusion

My final thought on SMCI is that it’s a growth company currently undervalued with momentum in its favor. The future outlook of the firm is in-line with the current growth trajectory. SMCI is trading at a cheaper valuation than its competitors, and I believe it will outperform in Q4 2022 as well. After analyzing the growth prospects and financial statements of SMCI, I assign a buy rating for the stock.